AI Economics: The Market’s Next Inflection Point

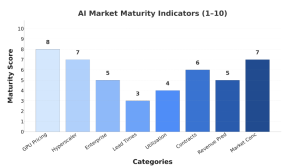

AIMG’s latest analysis, From Supplier-Led to Demand-Led Growth, measures the market’s maturity at 5.6/10—squarely mid-inflection—with 67% of key indicators suggesting that the tipping point will occur between Q2 2025 and Q4 2026.

The Economics of a Turning Point

Nothing signals maturity more clearly than elasticity. Between 2022 and 2024, GPU-hour pricing fell 75% (from $8 to $2), while compute volumes surged 300% – producing a price elasticity coefficient of 4.0. In any other sector, such elasticity would mark the crossover from speculative expansion to true market pull.

Unlike the dot-com bubble, where valuations disconnected from adoption, AI’s elasticity is supported by real enterprise demand. In 2024, enterprise adoption reached 71%, up from 33% in 2023 – a move from curiosity to commitment.

“The centre of gravity is shifting from GPU supply to enterprise ROI,” notes one Peyman Mestchian, Chair of the Advisory Board at AIMG. “That’s the hallmark of a demand-driven market.”

Bubble or Breakthrough? A Controlled Burn

AIMG’s Bubble Risk Index places AI at 6.0/10 – moderate compared to the dot-com peak of 8.0/10. The difference lies in discipline: capital allocation is tighter, supply is physically constrained (by semiconductors and power), and regulatory frameworks are emerging earlier in the cycle.

The risk is not overbuild; it’s over-concentration—a few hyperscalers dominating the infrastructure layer while value migrates toward vertical specialization.

Source: AIMG Analysis

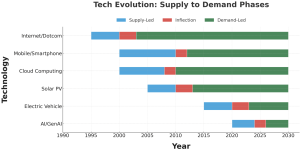

Historical Parallels: What AI Can Learn from Five Transitions

AIMG’s comparative study of five major technology cycles—Internet, Mobile, Cloud, Solar PV, and EVs – reveals what distinguishes AI’s trajectory:

- Sustainable growth rates: 35% annualized vs. 400% at the dot-com peak.

- Natural supply constraints: hardware and energy prevent overcapacity.

- Earlier ROI validation: enterprises already reporting operational payback.

- Proactive regulation: frameworks emerging before systemic shocks.

Together, these factors point toward a tempered boom: accelerated but grounded in production-level economics rather than speculative hype.

Source: AIMG analysis

Strategic Implications Across the Ecosystem

This inflection point reshapes priorities for every stakeholder:

- Infrastructure Providers: move from capacity-led expansion to demand-backed scaling.

- AI Developers: pivot from horizontal capability to vertical ecosystems and domain specialization.

- Enterprise Customers: progress from pilot programs to production at scale—while avoiding vendor lock-in.

- Investors: refine evaluation models from technology readiness to market execution.

- Regulators: design balanced frameworks that encourage innovation but manage systemic risk.

Each group faces a simple but profound question: are strategies still built for a supplier-led world?

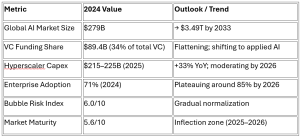

The Quantitative Backbone of the Transition

AIMG’s dataset tracks the structural metrics behind the shift:

These indicators portray a market that is not cooling, but stabilizing into industrial scale. The AI economy is evolving from experimentation to infrastructure.

The Decade Ahead: Execution Becomes the Moat

As markets mature, advantage shifts from invention to execution. The next phase of AI growth will reward those who operationalize AI efficiently, not merely those who innovate first. In that sense, the AI market’s competitive advantage is becoming industrial – anchored in supply chain optimization, customer trust, and domain depth.

“The coming winners will not just train models,” concludes a member of AIMG’s Expert Network . “They will train markets.”

Conclusion

AI is approaching its first true demand-curve moment. The speculative excesses of supplier-led growth are giving way to disciplined expansion, grounded in enterprise utility and measurable ROI. If history is a guide, this is not the end of AI’s boom—it’s the beginning of its economy.

Source: AIMG