The AI Commercial Blueprint – Harnessing Proprietary Market Intelligence to Drive Category Ownership

The AIMG Enterprise AI 2026 benchmark study of 2,048 enterprise decision-makers globally confirms it: 87% of organizations now use AI in at least one function, up from 66% in 2021. Generative AI adoption has reached 70% of enterprises, representing the fastest technology adoption velocity in enterprise software history.

Yet the ROI tells a different story. Deployment without strategic intent rarely produces lasting returns.

- 79% of enterprises report no measurable EBIT impact despite near-universal adoption

- Only 19% of organizations are fully data-ready to scale AI beyond one to three use cases

- Agentic AI is scaling fast: 22% of organizations are already there, with 41% of enterprise applications projected to include AI agents by year-end 2026

The window to build the intelligence infrastructure underneath it is closing and 2026 will be the year of implementation reckoning.

The reason is hiding in plain sight. Most organizations deploy AI tactically, squeezing efficiency from existing operations across functions. The tools make execution faster. They do not make the decisions driving it smarter.

Most AI vendors repeat their clients’ mistakes. They treat AI as a production tool when they need an intelligence teammate, one that reads the market on their behalf and directs GTM before the first dollar. That is what this piece is about: the winning blueprint for decision dominance.

SHIFTING FROM ATTRIBUTION TO INTELLIGENCE

For the better part of two decades, B2B commercial organizations operated on a single intelligence principle: attribution. Campaigns ran, conversion events were measured, and GTM motions were refined backward from closed-won outcomes. This model worked when information asymmetry favored vendors and the constraint on commercial reach was production capacity.

Generative AI has eliminated that scarcity entirely. Any vendor can now produce campaigns, content, and personalized outreach at scale in hours. The constraint is no longer production. It is decision precision: knowing which accounts are ready to move, which messages will land, and where the GTM motion should be directed before the first dollar is spent.

Attribution tells you what worked. Signals tell you what is working now, and how to educate your buyers more precisely in real time.

Attribution, by design, is a batch system. It processes completed interactions and reports backward on performance. Commercial decisions, however, are made in real time, in live conversations, active deals, and shifting buyer intent.

The gap between the two is where most AI-enabled GTM motions break: organizations are making real-time decisions using batch-processed data. By the time attribution confirms what worked, the window on the next account has often already opened and closed. The intelligence layer has to move upstream: before the campaign, before the strategy, before the first dollar of spend.

There is a deeper problem specific to this category. Enterprise AI buyers are not experienced purchasers. They are making a genuinely novel decision about how their organization will think, process information, and operate at scale, and their critical thinking is actively developing as the buying process unfolds. The questions they ask in discovery call one are materially different from the questions they ask in discovery call three. Not because they are being difficult, but because they are figuring out what they need to ask in real time. Behavioral data from past interactions captures an earlier version of that thinking, one the buyer has already moved past. Live conversation signals are the only intelligence that actually keeps pace with where the buyer is now.

This is not a niche dynamic. AIMG’s research confirms that insufficient talent and skills (4.65 out of 5.0) and model governance and transparency (4.55) now rank as the top barriers to AI value realization. Buyers are navigating complexity they do not yet have the institutional vocabulary to describe. The vendor who builds the architecture to listen, synthesize, and respond to that evolving buyer language in real time holds a structural advantage no campaign budget can replicate.

Signals, in this context, are patterns confirmed by frequency across your own conversation data: the same question surfacing in five separate discovery calls across unrelated accounts, the same objection recurring in customer success interactions that never reaches the positioning team, the same competitive name appearing in partner conversations without ever entering your CRM. Each instance alone is noise. The pattern is intelligence.

When that intelligence is operationalized, the commercial impact is direct and measurable. In practice, this has translated into sales cycle compression of approximately 50%, earlier buyer self-qualification driven by precise messaging, and the ability to pivot positioning within 72 hours when a signal repeats across five or more independent conversations.

Sales time concentrates on deals that are genuinely moving because the intelligence layer has already filtered noise upstream. Pipeline velocity improves not because headcount or spend increased, but because the decisions informing the GTM motion got smarter.

The shift in reporting follows. MQL volume measures the output of a push motion. Pipeline velocity measures the efficiency of an intelligence-driven motion against revenue outcomes. For boards evaluating commercial momentum and exit readiness, these are not equivalent measures. One reports activity. The other reports trajectory. This distinction mirrors the broader shift AIMG identifies across the enterprise AI market: from batch reporting of past performance to real-time intelligence guiding live decisions. The organizations that have made this shift are the ones appearing in the 21% generating measurable EBIT impact. The rest are still optimizing execution.

BUILDING THE INTELLIGENCE BLUEPRINT

Every AI vendor is already generating the raw material for an intelligence-driven GTM motion. It exists in discovery call transcripts that are recorded but never systematically synthesized. In partner conversations that

surface competitive intelligence and evaporate the moment the call ends. In repeated objections that live in individual sales reps’ institutional memory and disappear when they leave. In customer success interactions that reveal exactly where AI adoption is stalling, but never travel back to the teams responsible for positioning.

The intelligence layer is the architecture that captures, synthesizes, and operationalizes this intelligence before commercial strategy is set, not after campaigns have run. It is not a reporting function. It is a pre-strategy system that treats every customer-facing conversation as a signal source and every repeated pattern as actionable market intelligence.

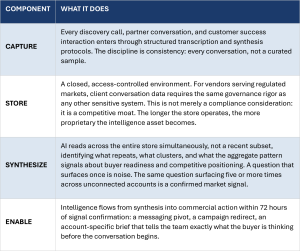

The intelligence layer has four components that must function as an integrated system:

In my experience building this architecture across PE-backed technology companies, three patterns emerge consistently:

- The intelligence was already there. The signals existed inside the business long before the system did. The architecture made them visible for the first time.

- Commercial teams closed faster because the content was exact. Prospects self-qualified earlier: the messaging was so precisely matched to what buyers were already thinking that the conversation started further down the funnel.

- The advantage compounds because the asset deepens. Every quarter the system runs, your institutional knowledge of what buyers are thinking, asking, and resisting grows more complete and more proprietary. Competitors starting later are not just behind. They are building on a permanently thinner foundation.

LEVERAGING INTELLIGENCE TO CREATE CATEGORY OWNERSHIP

That deepening institutional knowledge has a consequence most AI vendor CMOs have not yet fully acted on. It is not just a commercial advantage. It is the raw material for owning the narrative of the market they serve.

Most AI vendors are competing for market share. The ones building the intelligence layer are accumulating something more valuable: proprietary market intelligence, a systematically built, continuously compounding window into what buyers across their entire market are actually thinking, asking, and struggling with in real time. Every discovery call, every partner conversation, every customer success interaction adds to it. As the category evolves and buyer sophistication deepens, so does the asset. No competitor starting later can replicate the longitudinal signal of a system that has been listening for years.

AIMG’s research makes the stakes concrete. Financial services leads enterprise AI adoption at 89%, with fraud detection, credit risk, AML, and trading driving deployment. Risk management and compliance rank as the highest AI investment priority across all business functions, scoring 95 out of 100. These are not early adopters experimenting at the margins. They are institutional buyers making consequential, multi-year infrastructure decisions. The vendor who enters those conversations already knowing what questions this buyer class is asking across dozens of prior engagements is not selling the same way as everyone else. They are operating from a different information layer entirely.

That intelligence is not just a sales tool. It is publishable. It is the basis for the point of view that defines how the category is understood, what the right questions are, and what good adoption actually looks like. The vendor who builds the intelligence layer is not just closing deals smarter. They are positioned to set the terms of the conversation their entire market is having.

Category leaders do not just respond to the buyer journey. They shape it, by harnessing market intelligence patterns that tell them what buyers need to hear before buyers know how to ask for it.

Investors and boards already know this. Category ownership signals defensibility, pricing power, and reduced competitive exposure. It moves multiples. It is the difference between a company that sells into a market and a company that defines one. The CMO who builds the intelligence layer is not just driving pipeline. They are building the asset that makes the company more valuable to acquire, invest in, or take public.

Which raises a question the market has not yet answered: if proprietary market intelligence, a closed, compounding store of market signals from thousands of buyer conversations, is more defensible than most technology IP, appreciates rather than depreciates, and directly drives the commercial outcomes that determine enterprise value, why is it not being valued the same way?

Technology IP sits on the balance sheet. Proprietary market intelligence does not. Yet. The CMOs who build it first will define what it is worth.

THE BLUEPRINT FOR CATEGORY OWNERSHIP: WHERE TO START

Three practical steps follow from the analysis above.

First, reframe where intelligence sits in your commercial sequence. Attribution sits after execution. Intelligence sits before strategy. Until your GTM motion is informed by synthesized signals from your own conversation data, you are optimizing execution rather than directing it. AIMG’s data is unambiguous on this point: the organizations scaling AI toward measurable business impact are the ones who built the data and governance infrastructure first. The same principle applies to commercial intelligence. You cannot synthesize signals from data you have not been capturing.

Second, replace lead scoring with frequency-based signal detection. Lead scoring was the most sophisticated approximation available when direct access to buyer intent was not architecturally possible. The intelligence layer makes the proxy unnecessary. When the same question surfaces repeatedly across separate accounts at separate stages of the buying process, you have intent directly, expressed in the buyer’s own language, confirmed by frequency. The market is doing the scoring.

Third, change the metrics you report to the board. Pipeline velocity, adoption cycle compression, and signal-to-close conversion rates are more accurate leading indicators of commercial health than MQL volume or campaign conversion rates. Boards evaluating AI companies for exit readiness should be asking for these metrics. AIMG identifies this shift explicitly: the organizations moving from ad hoc AI pilots, down from 36% in 2021 to 12% today, to enterprise-wide strategic programs, up from 22% to 56%, are the ones building governance and measurement infrastructure that scales. The commercial intelligence layer is the GTM equivalent of that infrastructure shift.

The gap between enterprise AI investment and enterprise AI commercial outcomes is not closing on its own trajectory. The organizations compounding commercial advantage in this market share one architectural characteristic: they built the intelligence layer before they built the strategy. They listened before they spent.

The market is already generating the signals AI vendors need to win it. The organizations that harness them systematically will not just close more deals. They will own the conversation their entire market is having. That is what proprietary market intelligence builds. And it starts with the decision to listen.

Judith M. Peterson is a CMO and AI GTM strategist, with five PE-backed exits totalling $25B+ in transaction value. She serves on the AIMG Advisory Board.